|

What are the controversies surrounding the federal budget and the tax system?

The major controversies are the following:

- The necessary tax level

- Whether deficits should be tolerated

- Whether the tax burden should be primarily on the wealthy

What is our present tax level?

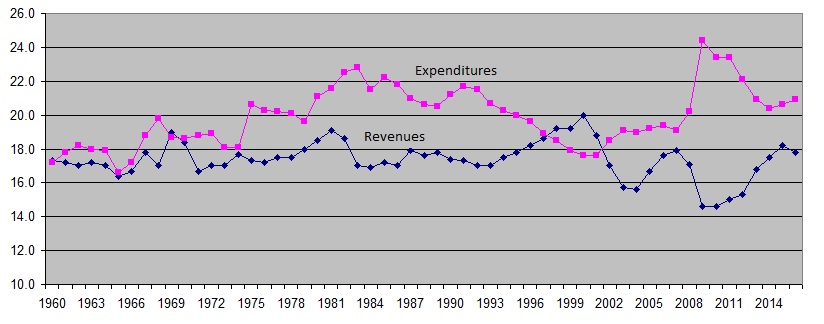

Because our government responsibility is divided between the federal government, the states, and local government; taxes are collected by all of these branches. The income tax is the principal tax collected by the federal government. As measured by the Gross Domestic Product, the federal tax level ranged between 17% and 20% during recent decades until it precipitously dropped under the 17% level because of the Bush Administration tax cuts. Revenues are now at a modern time low of 15% of the GDP while expenditures have skyrocketed primarily due to the financial bailout.  (Click to see chart) Although states vary significantly, the sales tax is the most common state tax. (Click to see chart) Although states vary significantly, the sales tax is the most common state tax.  (Click to see chart) Local governments assess a real property tax. (Click to see chart) Local governments assess a real property tax.

How much tax is necessary?

Obviously, the federal tax level must bear a direct relationship to the federal budget.

The Federal Budget is presently $3.8 trillion which represents about 20 percent of the gross domestic product. Contrary to common perceptions, the cost of the federal government when compared to the GDP has steadily decreased from a peace time high of 23.5 percent in 1983. What has changed is the nature of the expenditures. Defense expenditures have gone down while Social Security, Medicare and interest expenses have gone up. One reason for the increase in Social Security portion of the budget is that there are far more retirees entitled to Social Security benefits now then there were in the 60s. Interest payments were 6% to 8% of the budget from the '60s through the '70s. This percentage began to steadily increase as a result of the growing deficit to a high of 15.4% in 1996.

When the state and local government sector of the economy is added, the total government portion of the GDP is between 25% and 30%. This rate of government spending and revenue is approximately equivalent to Japan and far less than Canada and other European countries.

Why is there a budget deficit?

Quite simply, a budget deficit occurs when taxes do not generate enough income to cover the costs of government programs. Unlike many states, the federal government is under no mandate to balance the budget on a yearly basis. To a certain extent, government revenues are dependent on the state of the economy. If the economy is robust and there is low unemployment, more people will have taxable income and revenues will increase. Conversely, when there is high unemployment, tax revenues will decrease but government spending will not correspondingly decrease unless Congress cuts spending programs. In recent decades, there has a lack of political will to match revenues with spending. Beginning with the Reagan presidency in the 1980's, tax reductions and massive military spending combined to create a continuing deficit. The continued expansion of the debt contributed to making the debt a major issue in the 1992 Presidential campaign. Subsequent to the election, Congress raised taxes. These additional revenues together with the booming economy of the '90s generated enough new tax collection that a brief budget surplus was created. In response to this surplus, Congress accepted much of President Bush's proposal for tax relief and passed a major tax reduction package in 2001. Now there is no longer a budget surplus and the budget deficit is growing faster than projected. But the budget deficit has not yet regenerated the earlier concern regarding its size. Legislation measures lifting the debt "ceilings" that Congress has imposed on itself regularly pass. After years of relative public apathy regarding the issue, Americans now consider the deficit issue equal to the threat of terrorism in national importance.

How should the tax burden be split?

Generally speaking, the income tax is a progressive tax which means that individuals with larger incomes bear a larger tax burden. The degree to which the tax is progressive has fluctuated significantly in the past two decades and more of the tax burden has shifted to the middle class. From the mid-1960s until 1982 the tax rate ranged from about 15% for the lowest brackets to about 70% for the highest. Because of significant inflation during this period, many in the middle class entered the higher tax brackets even though politicians boasted that there were no tax "increases". In 1982, Congress passed President Reagan's plan to cut the highest rate on personal income tax from 70% to 50%. The Tax Reform Act of 1986 dramatically lowered the maximum tax rates from 50% to 28%. This was increased to 31% in 1991, and additional rates of 36% and 39.6% for the wealthiest individuals were approved in the Omnibus Budget Reconciliation Act of 1993. Under President George W. Bush's tax proposal the maximum tax bracket would be reduced to 33%. The ultimate tax package agreed to by Congress has reduced the maximum rate to 35%.

Because the Social Security tax is not progressive, and because there are lower marginal rates for certain types of income, the actual effective tax share for middle income wage earners is far greater than that of lower and upper income earners.

What is the concern about the alternative minimum tax?

To make sure that everyone paid at least a minimum of taxes Congress enacted the

individual alternative minimum tax (AMT) in 1969. Historically, the AMT has only affected taxpayers at the highest income levels. However, because the AMT is not indexed by inflation, that is about to change. Preliminary estimates indicate that by 2010, when the effects of both inflation and the 2001 tax cut are taken into account, at least one third of all taxpayers will be affected and the overall liability of these taxpayers will be significantly increased. Ironically, the tax cuts contained in the new legislation will increase the number of taxpayers affected by the AMT. Congress has not responded to calls for the AMT to be "indexed" as ordinary marginal tax rates are. Instead, under the 1991 tax act, the AMT exemption was temporarily increased by $4,000 for joint returns ($2,000 for unmarried individuals) effective for tax years between 2001 and 2004. In tax year 2005, the AMT exemption amount reverts back to its previous levels. Certain tax credits were also permitted to be be applied against AMT liability.

What is the status of the estate tax?

The estate tax has been a permanent part of the federal taxation system since 1916. The current estate tax consists of the traditional estate tax, plus two additional components designed to close "loopholes": a gift tax and a generation-skipping transfer (GST) tax. The gift tax requires that all taxable gifts made during life by the deceased be included when calculating the value of the estate. The GST tax captures wealth transfers that "skip" a generation, such as a trust that a grandmother leaves to her grandchildren. The value of all three types of wealth transfers are aggregated and taxed together at rates effectively ranging from 37 to 60 percent on net taxable estates.

Because many exemptions and deductions, only a very small percentage of taxpayers are affected by the estate tax and gift tax. In 1997, the estates of fewer than 43,000 people - fewer than 1.9 percent of the 2.3 million people who died that year - had to pay any estate tax. The Joint Committee on Taxation projects that the percentage of people who die whose estates will be subject to estate tax will remain at about two percent for the foreseeable future.

The complete repeal of the estate tax as long been a Republican cause. The Bush tax cuts slated the estate tax for extinction beginning in 2010. But the Democratic controlled Congress has voted to revive the tax after a one year hiatus in 2010. The Senate has not acted on the measure.

What are the arguments in favor of and against the repeal of the estate tax?

Repeal of the estate tax was a significant part of President Bush's present tax cut proposal. This proposal was opposed by most Democrats and a growing number of concerned wealthy Americans who are particularly concerned about the affect of the repeal on charitable giving.

The proponents of the repeal contend:

- The existence of the estate tax this century has reduced the stock of capital in the economy by approximately $497 billion, or 3.2 percent.

- The incentives in the estate tax result in the inefficient allocation of resources, discouraging saving and investment and lowering the after-tax return on investments.

- The estate tax is extremely punitive, with marginal tax rates ranging from 37 percent to nearly 80 percent in some instances.

- The estate tax is a leading cause of dissolution for thousands of family-run businesses. Estate tax planning further diverts resources available for investment and employment.

- The estate tax obstructs environmental conservation. The need to pay large estate tax bills often forces families to develop environmentally sensitive land.

- The estate tax violates the basic principles of a good tax system: it is complicated, unfair and inefficient.

The opponents of the repeal maintain:

- the estate tax helps reduce concentrations of wealth and power

- there would be a significant loss of revenue if the estate tax is repealed

- repealing the estate tax would reduce charitable bequests. They believe that the estate tax has encouraged families with estates in excess of $20,000.00 to bestow an average of 40% of the estate to charity and that this percentage would be significantly reduced if the estate tax was repealed.

- farms and small businesses can be protected without repealing the estate tax

How do other countries handle taxes?

With the exce

ption of Japan (which is at approximately the same level as the United States), the tax level and the corresponding cost of government is much higher in most other industrialized countries. The income tax is more significant in the United States than other countries and raises 50% of all government revenue. In most other major countries, a large amount of revenue is raised by a "Value Added Tax" which is similar to a sales tax but is assessed at the time goods are manufactured and when they are distributed and sold. Most industrialized countries also have estate taxes but this tax accounts for a very small part of the overall revenue. Although there has been concern about the national debt, the size of the United States public debt is not excessive when compared to some other industrialized countries.

How do Democrats and Republicans stand on tax issues?

There is a wide difference between the two parties. Republicans favor lower taxes and low marginal rates for the wealthy. Republicans overwhelmingly supported the tax package passed by Congress in 2001 whereas it was opposed by most Democrats.

Democrats supported the 1993 legislation which raised the maximum tax rate.

Tax and Budget Links

Google Directory - National Budget

Google Directory - Taxation

Wikipedia - Federal Budget

Wikipedia - U.S. Taxation

Wikipedia - Federal Budget

Wikipedia - Income Tax

Wikipedia - Sales Tax

Wikipedia - Estate Tax

Wikipedia - Alternative Minimum Tax

Census Bureau - State and Local Government Finances

Citizen's Guide to the Federal Budget (The link is to documents from prior years. The Bush and Obama Adminstrations have unfortunately stopped updating this excellent and understandable summary)

Open Directory Project: National Budget

Center on Budget and Policy

Priorities

|