|

What are the latest developments regarding tort reform?

A major national Republican victory in its efforts to achieve meaningful tort reform occurred in February 2005 when Congress approved a class action reform measure. See Senate vote See House vote . The legislation authorizes federal courts to hear class-action suits involving over $5 million and involving persons or companies from different states. The objective in moving the suits to federal courts is to make it significantly more difficult for the lawsuits to be approved. The bill would also crack down on "coupon settlements" in which plaintiffs get little but their lawyers get big fees. It would link lawyers' fees to the amount of coupons redeemed. But national efforts at other reforms, such as medical malpractice reform and establishing an asbestos trust fund, have fallen short. There continue to be legislative achievements at the state level on tort reform issues.

Tort reform remains a major policy objective of the Republican party. The 2008 Republican platform continues the pledge to reform what is described as corruption in the civil litigation system. Democrats are basically in a defensive position on the issue.

"Tort reform" is a major part of the Bush Administration's domestic agenda. What are torts? Until "tort reform" became a policy issue, the word "tort" was primarily the part of the vernacular of first year law students. Technically, a tort is any civil wrong in which a damaged victim can seek legal redress from the individual who caused the harm. In its political context, "tort reform" generally refers to proposals to limit the prevalence of legal claims prosecuted with the assistance of personal injury lawyers which are perceived to unfairly burden insurance policy holders with exorbitant premiums. Tort law, like most of our legal system, is traditionally a matter of state "common law" and legislation. But Bush Administrative legislative initiatives seek to partially modify this by imposing uniform limits applicable to all states.

In actuality, the "tort system" is part of an overall system for compensating victims who suffer from accidental injuries. Accidents are a part of our human experience. Studies indicate that over the course of a year, approximately 20% of Americans suffer some type of accidental injury and most of these require a doctor's attention.  (Click to see chart) The vast majority of accidents causing economic loss are either work-related or automobile-related. Many of these accidents do not involve potential liability of a third party. The primary source of compensation for medical treatment of these injuries is the victim's health insurance. (Click to see chart) The vast majority of accidents causing economic loss are either work-related or automobile-related. Many of these accidents do not involve potential liability of a third party. The primary source of compensation for medical treatment of these injuries is the victim's health insurance.

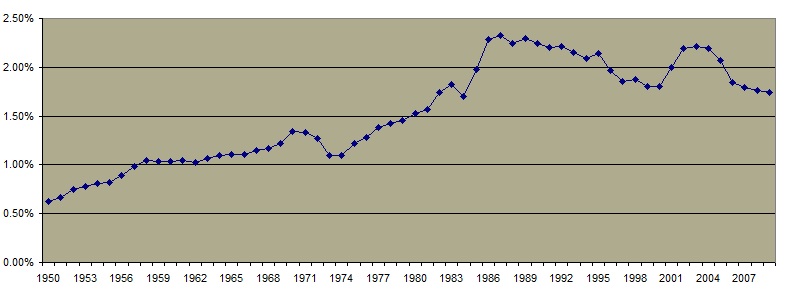

To the extent that compensation is provided through legal claims, critics of the present tort system maintain that it is too expensive and inefficient. Over 60 years, the per capita annual costs of the tort system have increased significantly.

Even when non-economic "pain and suffering" awards are included, it has been estimated that claimants ultimately collect only 46 percent of the total cost of the tort system. Tort costs, as a percentage of the GDP, exploded in the decades of the '70's and '80's. There has been a slight decrease in recent years due mainly to legislation in several states. The system is also not even-handed. An important variable in determining the value of a given personal injury claim is the locality where the claim is filed. A case with the same type of liability and injury can be worth variable amounts in different jurisdictions. This factor accounts for much of the regional variance in insurance rates.

Even when non-economic "pain and suffering" awards are included, it has been estimated that claimants ultimately collect only 46 percent of the total cost of the tort system. Tort costs, as a percentage of the GDP, exploded in the decades of the '70's and '80's. There has been a slight decrease in recent years due mainly to legislation in several states. The system is also not even-handed. An important variable in determining the value of a given personal injury claim is the locality where the claim is filed. A case with the same type of liability and injury can be worth variable amounts in different jurisdictions. This factor accounts for much of the regional variance in insurance rates.

Proponents of the tort system argue that it deters accidents by combining compensation for victims with negligence. They also maintain that the system provides necessary compensation for victims who would not otherwise be sufficiently compensated by other social insurance programs.

What has caused the increase in liability costs?

- Expanded bases of liability

Until about 20 years ago, a plaintiff was required to show a complete absence of personal negligence in order to recover. This "contributory negligence" rule significantly limited the number of injured persons who could claim damages. Today all but a handful of states have a "comparative negligence" standard which allows an apportionment of damage based on degree of liability. In most states, the plaintiff must be less at fault than the defendant.  There has been expansion of liability in other areas as well, such as product liability. There has been expansion of liability in other areas as well, such as product liability.

- Increase in number of lawyers

Many critics of the current system suggest that the increased use of the tort system has been driven by an increase in the number of attorneys. The number of lawyers has increased at a rate which far exceeds population growth. The number of lawyers per capita varies significantly from state to state. The expansion of legal employment opportunities has occurred throughout the legal field. In particular, there has been a major increase in the divorce rate and in criminal cases. Still, personal injury litigation is a common practice specialty for lawyers, accounting for about 25% of the legal workload in many states.

- Increase in legal specialization and technology

Like other professions, the law profession has undergone significant specialization in recent years and has significantly benefited from technological advances. This has enabled lawyers to more efficiently process cases. The specialization has also enabled practitioners to become successful in areas demanding significant expertise such as medical malpractice and product liability.

- The investment market

A unique feature of liability and casualty insurance is that the premium is received long before the losses occur. This provides the insurance company the opportunity to profitably invest the premiums. Insurance premium rates are thus not only dependent on actuarial risk factors but also the degree to which premiums can be profitably invested. In times of slow economic growth and low interest rates, it is inevitable that premium amounts will increase even if potential losses are not increasing.

- The contingency fee system of compensating attorneys

Plaintiff's attorneys are compensated by the "contingency fee" system in the majority of cases. Under this method of compensation, the attorney bears the full cost of trial preparation and is paid only if a favorable result is obtained. Critics argue that this system encourages lawsuits and limits the degree to which successful plaintiffs can obtain relief. Proponents of the contingency fee system maintain that without it, most injured victims would be unable to obtain relief. Salary surveys have revealed that the compensation of personal injury plaintiff attorneys is not significantly different than other practicing attorneys. The overall cost of plaintiff's attorney's fees constitutes approximately 19% of total tort costs, an amount slightly larger than defendant's attorney fees.

- Promotion of Attorney Services

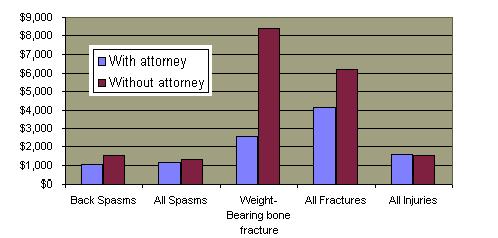

Prior to a Supreme Court decision in 1977, attorneys were prohibited from using paid advertisements to promote their services. Today, advertisements for attorney services are abundant and solicitations for personal injury services are most prominent. Although most plaintiffs find attorneys through a referral , the advertising has a cumulative effect of persuading prospective personal injury litigants of the desirability of hiring an attorney to get maximum benefit. Interestingly, a 1991 study indicated which surveyed attitudes of persons who filed claims, found that the satisfaction rate was significantly less when the claimant hired an attorney. Studies also indicate that for some types of injuries, policy holders are better off settling the claim without an attorney.

Why is medical malpractice reform a policy issue? There are many reasons. By the nature of their profession, doctors practice in an environment in which mistakes can create significant injuries. This has always been true, but legal actions against doctors did not become common until the last several decades. There has been a steady increase in overall costs. There are several reasons for the increase: greater specialization and expertise of plaintiff's attorneys, a more impersonal medical system in which victims are less reluctant to sue, and the emergence of medical experts who are willing to testify against doctors.

Malpractice premiums are a small portion of medical costs, even for doctors who practice in high risk specialties. But it is not just the financial cost of medical malpractice insurance that annoys doctors. It is understandably discomforting to have the quality of one's professional efforts dissected in an adversarial setting, particularly when the outcome was disappointing. A significant portion of claims filed (even some which are successfully settled or litigated) involve no negligence.

Studies indicate that only a small fraction of medical mishaps become legal malpractice claims. Although the vast majority of doctors are not sued, a study involving New York doctors indicates that about 40% who made malpractice payments have had multiple claims. Malpractice awards are brought against physicians, the hospitals, and other medical personnel. In recent years the number of malpractice payments has declined. The rate of such claims does significantly vary from state to state. There has been very little change in the average payment when adjusted for inflation over the past two decades.

Medical malpractice reform was at the forefront of the "tort reform" agenda of the Bush Administration because it combines the particular dissatisfaction of medical community with the overall concerns of insurers and businesses regarding the costs of the tort system.

What reforms are proposed for medical malpractice cases? The Bush Administration's reform proposals are based on a reform measure enacted by California in 1975. The House has approved this legislation but it has been stalled in the Senate. In 2006, a Senate measure failed to secure the necessary 60 votes to close debate. The principle features of the House bill are:

- Cap on non-economic damages

There would be separate caps for "non-economic "damages at $250,000. Virtually all medical malpractice awards include a substantial amount for "pain and suffering". It is this element of damages that would be limited. Although several states presently have medical malpractice "damage caps" of some type, only five states have the limit on non-economic damages proposed by this legislation. Although proponents of this legislation argue that California's similar provisions have successfully kept insurance rates down, the evidence suggests that it was insurance reform, not damage caps, that has truly affected California's malpractice rates.

- Limitation on attorney's fees

Plaintiff's attorney fees would be limited to (1) 40% of the first $50,000 recovered; (2) 33 % of the next $50,000 recovered; (3) 25% of the next $500,000 recovered; and (4) 15% of any recovery in excess of $600,000. About ten states presently have similar limits on attorney's fees.

- Allows consideration of "collateral sources" in measuring damages

In many states, juries are not informed about the extent to which injured patients may have already received benefits, usually through health or disability insurance policies. The proposed legislation will allow the jury to consider this information in determining damages. A majority of states already have similar rules pertaining to collateral sources.

- Mandates periodic payment of damages

The measure requires that all future damages over $50,000 be made in periodic payments. This substantially reduces the value of the award. Currently about a third of the states mandate periodic payments but most are at thresholds substantially in excess of $50,000.

How does the tort system interact with automobile liability? The tort system is the foundation for the settlement of claims resulting from traffic accidents. The controversies involving the tort system in general are certainly applicable to automobile liability. While there has been an overall decrease in the accident rate , automobile insurance costs have increased dramatically throughout the country. The notable exception to the trend is in California, where the rates are regulated through 1988 voter-passed legislation. This legislation also mandates a 20% "good driver" discount which has encouraged motorists to reduce the number of claims. Insurance costs are a substantial portion of household transportation expenditures. The annual cost of auto insurance ranges from a low of just over $500.00 in North Dakota to over $1100 in New York. Although all states mandate that drivers carry auto insurance, a substantial percentage of drivers remain uninsured which significantly increases the premium rates of drivers who are insured.

The percentage of bodily claims varies significantly from state to state.

Only about a third of auto injury victims who consider filing a claim actually hire a lawyer. The percentage of such claimants who retain a lawyer has increased in the last 20 years, but not significantly.

Sixteen states have attempted to address the problems associated with the traditional tort treatment of automobile liability with "no fault" insurance systems which removes effectively removes automobile liability from the traditional tort system. Three of these (Pennsylvania, New Jersey and Kentucky) offer motorists a "choice" between no-fault and the traditional liability system. Under "no fault" plans, injuries for all accidents are compensated regardless of fault but the amount of damages is regulated. The no-fault system has not lived up to its promise of lowering the cost of auto insurance as insurance rates in the majority of these states are above the national average. The New York no-fault system in particular has been plagued by fraudulent claims where "staged" accidents and "phantom" symptoms have been common. Despite the predictions of plaintiff lawyers, the adoption of "no fault" systems do not appear to have led to more negligence as there is no appreciable difference between no-fault states or tort states in the rate of fatally related accidents.

Most accidents are work-related. Are they compensated by the tort system? No. A "no fault" system called "Worker's Compensation" has been in effect since the 1920's to compensate such injuries. Worker's Compensation legislation was created because employers had used the tort system successfully to defeat many legitimate claims. Worker's Compensation is quite similar to "no-fault" auto insurance - it provides benefits to injured victims regardless of fault according to a regulated system of damages.

In all states but Texas, the programs are mandatory although there are exemptions in some states for small firms and agricultural employees. Although coverage is voluntary in Texas, over 80% of non-federal employees are covered. Nationwide, the coverage is split between state-operated companies, private insurers, the federal government (for federal employees), and employers who self-insure. The portion of Workers Compensation payments which constitute payments for medical costs has increased significantly in the past 40 years. Worker's Compensation costs, as a percentage of wages, have significantly decreased during the past decade. This decrease is directly related to the reduced incidence of work injuries. Most Workers Compensation claims involve temporary cash benefits only but most of the total dollars paid in benefits are for permanent, partial disability. The amount of temporary benefits varies from state to state. The amount of total benefits significantly increased from during the '80's but has leveled since. Much of the increase has been driven by the overall increase in the cost of health care.

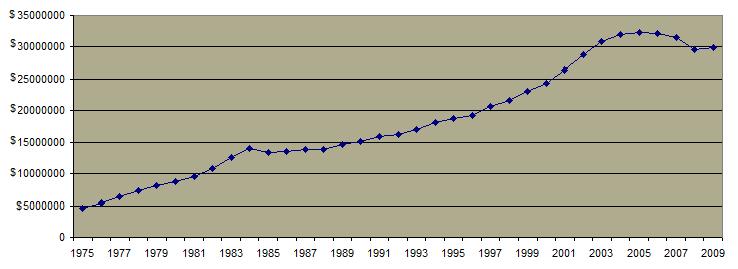

What about product liability and class actions? One of the major developments within the tort system during the past half-century has been the emergence of "product liability" lawsuits. These are suits brought by purchases of products were defective and which caused injury. This type of liability was the result of the mass marketing of consumer products, the increasing ability of plaintiff attorneys to understand the technical information necessary to prove these cases, and a growing "consumer awareness" on the part of the public. Changes in the law have also spurred this development of product liability. Until 30 years ago, it was necessary for a victim's lawyer to prove negligence in the manufacture of a product in order to impose liability. Recognizing that this was a significant burden, a series of state court decisions began to impose "strict liability" on product manufacturers if the product was shown to be defective. Today, all but a few states impose such a "strict liability" requirement. In the past decade, major jury verdicts have been reached in tobacco and pharmaceutical cases. To date, approximately $54 billion dollars has been awarded as compensation in asbestos-related litigation alone. The asbestos verdicts and settlements have caused the bankruptcies of a growing number of firms.

Quite often, product liability cases are brought as "class action" lawsuits involving multiple plaintiffs. The advantage of such class actions to plaintiff attorneys has been the ability to prove multiple cases of liability at the same time, thus leading to enormous verdicts. In California, class action construction-defect lawsuits have become very common for multi-unit developments, thus leading to a significant decrease in such housing at a time when overall California housing costs are exorbitant. California has passed legislation which provides contractors the opportunity to remedy such defects before a suit can be brought in the hopes of reducing this type of litigation. Perhaps the biggest concern is that plaintiff attorneys file such lawsuits in jurisdictions where large jury verdicts are routine. In 2005, Congress allowed defendants to move many of these lawsuits to federal court. (House vote) ; (Senate vote)

What is the controversy about "punitive damages"? Punitive damages can often be awarded in civil cases, including tort cases, where the defendant's conduct is found to be intentional or willful or wanton or malicious. For example, the financial verdict against O.J. Simpson primarily consisted of punitive damages. A few states prohibit the award of punitive damages and the majority of states which allow such damages require clear and convincing evidence. In addition, several states have placed limits on the amount of punitive damages which can be awarded (usually no more than a certain percentage of the compensatory damages). In ten states, a portion of the punitive damage award goes into a state fund.

Punitive damages verdicts are unusual; they are awarded in less than 4% of all tort jury verdicts where the plaintiff prevails. They are more common in financial litigation. Because most lawsuits are never go to trial and are settled, punitive damages are very small part of the tort system costs. But they are nonetheless controversial because they bear no relationship to compensation. Instead, they become a sort of windfall for the victim. The theory of punitive damages is to punish the perpetrator for particularly egregious conduct. It may be that such additional liability helps spur defendant companies to take remedial measures but it is difficult to measure whether this is true.

In 1996, Congress passed legislation which would have placed limits on the amount of punitive damages which could be awarded in products liability cases. The legislation also contained procedural measures which would make litigating these cases more costly. The legislation was vetoed by President Clinton. Similar legislation is expected to be considered again.

Why have states enacted "Joint and Several Liability" reform?

Tort defendants have long maintained that "joint and several liability" is inherently unfair and inequitable. Many tort actions involve multiple defendants. For example, a motor vehicle accident might involve the possible liability of not only a driver but also the government entity that constructed and allegedly unsafe roadway. Or a products liability matter might involve the seller, the manufacturer and any number of subcontractors. Medical malpractice actions typically involve the doctor and hospital as multiple defendants. Under the traditional concept of recovery, known as "joint and several liability", a single verdict is rendered against all defendants and the plaintiff is entitled to recover all of the damages from any defendant. The paying defendant then has recourse against other defendants for their share of the damage award. The practical effect of this procedure is that the defendant who has the "deepest pockets" generally bears the major burden of paying damages even though that defendant may have had contributed on slightly to the injury. Many states have completely repealed joint and several liability, others have modified it, and only a handful retain it.

What about victims of criminal behavior? One of the many anomalies of the tort system is that some of the most deserving victims have no way to recover. Perpetrators of crimes are liable for the damages that they cause but most are uninsured and incarcerated. Only recently have states developed comprehensive compensation programs for crime victims. The benefits issued by the states are supplemented by federal funds obtained through fines and forfeitures. Eligibility requirements for these programs are limited and most states have maximum payment levels which are relatively low compared to other compensation programs. The amount awarded in proportion to the overall crime rate significantly varies from state to state. Over half of the benefits compensate for medical and mental health expenses incurred by the victims.

How does the U.S. tort system compare to other countries?

This is difficult to measure. According to one study, the United States pays more than twice as much in tort costs than most industrialized countries. Although the U.S. has a favorable vehicle fatality rate in comparison to many countries , it is very difficult to conclude that the tort system has significantly contributed to this safety statistic. But there are fundamental legal and structural differences between most European countries and the U.S. with respect to compensation. Contingency fee arrangements are often not allowed and there are other procedural obstacles to recovery. The most important of these is that in virtually all legal systems except the U.S., the loser of a claim must pay the winner's attorney fees. On the other hand, European social insurance systems provide victims with far more comprehensive medical and financial benefits than comparable U.S. programs. New Zealand and Switzerland have abolished their tort law system and have adopted comprehensive "accident" programs to compensate all injured persons.

How do Democrats and Republicans stand on tort reform issues? "Tort Reform" is a very partisan issue. At both the state and national levels, Republicans overwhelmingly support tort reform and Democrats oppose it. The trial lawyer associations which represent plaintiff lawyers are major contributors to the Democrats. Insurance and medical interests contribute heavily to Republicans. In fact, the tort reform debate can be considered as an aspect of the overall political dynamic involving distribution of the nation's wealth. The most contentious issues involve medical malpractice and product liability. The result of settlements and verdicts of these cases is a transfer of wealth from groups which tend to be wealthy to victims and their lawyers. Virtually all the reform proposals ultimately attempt to limit the amount of funds which are distributed in this fashion.

More Information on Tort Reform

Pro-Reform:

American Tort Reform Association

Freedom Works - Lawsuit Abuse

Manhattan Institute Center for Legal Policy

Overlawyered.com

Anti-Reform:

Public Citizen: Civil Justice and Legal Rights

The Foundation for Taxpayer & Consumer Rights

Center for Justice and Democracy

Notable studies, articles:

Rand Institute for Civil Justice (Think tank specializing in research of civil

justice issues)

House Report: Improving the American Legal System: The Economic Benefits of Tort Reform

Tillinghast - Towers Perrin,U.S. Tort Costs: 2002 Update

Thomas F. Burke: Lawyers, Lawsuits, and Legal Rights, The Battle over Litigation in

American Society

Consumer Federation of America: "Why Not The Best? The Most Effective Auto Insurance

Regulation in the Nation" (An examination of the effects of California's Proposition 103)

Herbert M. Kritzer: "Seven Dogged Myths About the Contingency Fee"

Congress, Office of Technology Assessment "Impact of Legal Reforms on Medical Malpractice Costs"

Than N. Luu: "Reducing the Costs of Civil Litigation"

Todd J. Zywicki: "Public Choice and Tort Reform"

Reed Neil Olsen:"The Efficiency of Medical Malpractice Law

Theory and Empirical Evidence"

COMMITTEE FOR ECONOMIC DEVELOPMENT: "Breaking the Litigation Habit"

National Association of Crime Victim Compensation Boards

Department of Justice: Office for Victims of Crime

|